Key Takeaways

- Performance degradation in live trading is often driven by execution-related factors that traditional drift detection frameworks fail to observe.

- Execution assumptions embedded in backtests can quietly diverge from real-world market behavior, eroding alpha without any obvious signal decay.

- Transaction cost analysis (TCA) provides a critical diagnostic layer for distinguishing true model drift from changes in liquidity, venue dynamics, or market microstructure.

- By comparing expected and realized trading costs in near real time, firms can detect performance drift earlier and shorten the feedback loop between research and production.

- Integrating TCA into trade-lifecycle analytics improves attribution, reduces unnecessary recalibration, and extends the productive lifespan of successful strategies.

This blog explores the transformation of TCA (transaction cost analysis) from a post-trade reporting tool into a live diagnostic engine, offering immediate insights into market conditions and execution performance.

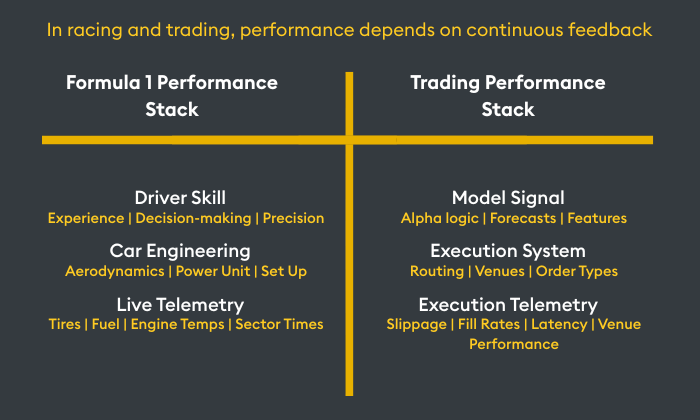

In the 2011 Canadian Grand Prix, Jenson Button overcame penalties, punctures, and torrential rain to make a miraculous comeback. Passing Sebastian Vettel on the final lap demanded a lifetime of practice at executing under pressure. Of course, McLaren engineers had spent just as long perfecting the car itself. But neither elite driving nor elite engineering alone secured the win; success also depended on the team’s ability to monitor real-time performance, detect issues, and adapt as conditions evolved.

It’s a lesson that should resonate with today’s hedge funds, racing for advantage in markets that are faster and more unforgiving than ever. With roughly 30,000 firms operating globally, edge isn’t just harder to find — it’s harder to sustain. Markets adapt quickly, alpha decays in days, and macro volatility, fragmented liquidity, and shrinking execution windows make for an increasingly treacherous operating environment.

When the rubber hits the road and quants push models into production, performance rarely fails catastrophically — it drifts. To combat alpha decay, firms need to spot underperforming models early and adjust them quickly before there’s a significant P&L impact. However, they also need to accurately assess what’s causing model degradation in the first place.

To close the gap between research and production, most drift detection frameworks focus on regime shifts, feature drift, model misspecification, or prediction accuracy. However, few frameworks monitor execution behavior.

The result is a critical blind spot. In Formula 1 terms, it’s like monitoring the car and the track, but not the race telemetry. Execution-driven drift — where execution behavior diverges from assumptions baked into research — can easily cause a strategy to underperform and compound into material P&L volatility, especially in high-frequency trading. Worse, misattributing these issues to signal decay or model failure can cause firms to retire sound strategies or waste time on unnecessary recalibration.

To distinguish execution-driven drift from common model or market effects that impact performance, firms need another layer of insight. This comes from live transaction cost analysis (TCA) that evaluates both direct and hidden execution costs — from slippage and fees to trade timing and market impact.

Execution assumptions are model assumptions

It’s no secret that quants are under pressure. The difference between leading and lagging the market now depends on how fast and effectively they can generate, validate, and deploy new ideas. In the race from research to production, backtests encode certain execution assumptions, but microstructure changes can cause varied forms of alpha decay. Depending on the particular desk, asset class, or execution style, firms can experience:

Rising slippage vs backtest assumptions

Backtests may encode fixed or regime-averaged cost assumptions, but live slippage can widen during volatility spikes or liquidity fragmentation. For instance, an intraday momentum strategy calibrated at 2bps may consistently realize 4bps in production, quietly eroding alpha despite unchanged signal timing and direction.

Fill probability deterioration

Strategies that rely on high passive fill rates can see execution quality degrade as liquidity thins or queue dynamics shift. If a model expects 95% fills in a passive FX carry strategy but realizes closer to 70% as liquidity migrates off primary venues during Asia hours, opportunity costs rise rapidly even though forecasts remain stable.

Venue-level performance drift

Changes in venue-specific liquidity, fee structures, price formation, or participant mix can degrade execution quality relative to research assumptions. The signal remains valid, but the venue no longer behaves as expected. For example, a VWAP routing strategy allocating flow to a crypto exchange where depth has thinned can systematically realize worse prices.

Latency-to-fill distortions

Routing delays, congestion, or infrastructure changes can push fills later into price moves, increasing adverse selection. Even millisecond-scale latency shifts can distort implementation shortfall in something like a triangular arbitrage strategy, where arriving just 30ms late collapses a previously exploitable price gap.

Most drift detection frameworks miss these sorts of execution-driven issues. One reason is siloed data: execution and research environments are usually separated in different systems; variables such as order size, pricing, and venue liquidity may not be centralized or easily accessible. Additionally, transaction cost analysis is often treated as a required reporting function rather than a vital diagnostic input, with batch-based interrogation happening post-trade, not live. Either way, the result is that useful insights are often omitted from drift logic.

How integrating TCA improves drift detection

While there’s no such thing as perfect execution cost modelling, TCA integration into drift detection can enable improved forecasts and more confident decisions, minimizing the gap between research assumptions and live trading conditions.

Live TCA can determine whether research assumptions still hold, enabling firms to distinguish between signal decay, shifting liquidity regimes, infrastructure or routing issues, and execution degradation. While not all firms have real-time or full-granularity TCA, many can incorporate some level of intraday execution metrics to complement and strengthen existing drift detection frameworks. This will be easier for some desks than others, with the fragmented and OTC nature of FX posing a particular challenge, but the principle applies across the board.

By comparing expected execution quality against realized fills, firms can detect divergence as it happens. This approach sorts true model or signal degradation from execution-related drift, enabling teams to make the right adjustments before small deviations compound into significant P&L volatility.

What does TCA-enhanced drift detection look like?

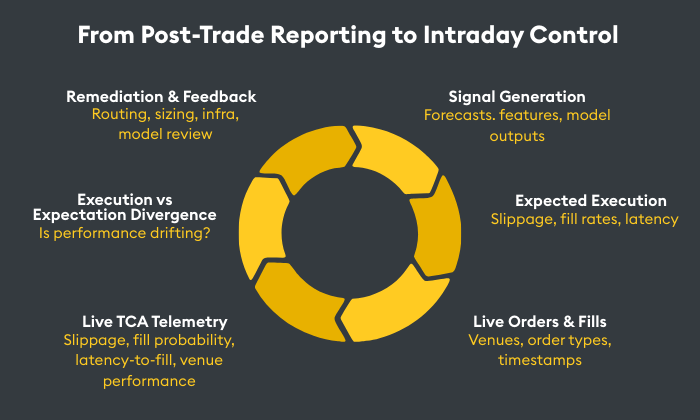

Implementing a TCA-enhanced drift loop requires unified, time-aware analytics that align signals, orders, fills, and market microstructure. This workflow transforms TCA from a post-trade reporting tool into a live diagnostic engine, offering immediate insights into market conditions and execution performance:

- Signal: A model detects short-term momentum in EUR/USD based on microstructure patterns.

- Expected execution: The backtest assumes 2bps slippage and a 95% fill rate for passive orders.

- Live fills: Trades are routed in real time. Fills arrive across multiple venues and order types.

- TCA metrics: Execution quality is measured against expectations: slippage, fill ratios, latency-to-fill, and venue-specific performance.

- Deviation detection: The system flags any divergence, such as spiking slippage.

- Remediation: Execution teams or algorithms adjust routing, order sizing, or strategy parameters. Research teams are notified if the issue persists, enabling faster model recalibration.

Closing this TCA-enhanced drift detection loop gives quants continuous visibility into execution fidelity, ensuring that model signals translate into real-world alpha even as market conditions and microstructure evolve.

Teams can rapidly triage performance issues, differentiating between execution degradation, signal decay, shifting liquidity regimes, or infrastructure issues. Backtests become more precise through continuous cost-model calibration, models gain robustness across regimes, and alignment between research and production improves — supporting quicker iteration cycles, less unnecessary recalibration, and a longer lifespan for successful trading strategies.

Outrun alpha decay

Amid turbulent markets and fragmented venues, static execution assumptions are no longer enough. TCA is fast evolving from a tick-box regulatory requirement or a retrospective reporting tool into a real-time diagnostic layer.

In practice, this evolution does not require heavy or opaque AI models. Many firms start by using lightweight, online learning techniques to continuously recalibrate execution expectations as trades are filled. Slippage, fill probability, and latency-to-fill assumptions can be updated intraday based on realized outcomes, allowing expected execution quality to adapt as liquidity conditions, volatility, or venue behavior shift.

Over time, these execution signals can also be used to support probabilistic attribution of performance degradation. By learning from historical execution patterns, teams can estimate whether underperformance is more likely driven by signal decay, changing liquidity regimes, routing inefficiencies, or infrastructure latency. This does not eliminate human judgment, but it materially shortens triage cycles by narrowing the space of plausible causes when strategies begin to drift.

Just as Formula 1 teams can’t rely solely on engineers to build the perfect engine or drivers to deliver flawless performance, hedge funds can’t only depend on sophisticated models and execution systems. They also need race telemetry: live TCA that shows how performance is evolving in the real world. Integrating live TCA into drift detection frameworks fills a critical blind spot in today’s hyper-competitive race for alpha, helping firms take the lead — and keep it.

Together, KX and OneTick connect quant research, trading analytics, and TCA on a single, high-performance data foundation. By unifying time-series analytics with tick-level market and transaction data, firms can keep research assumptions aligned with live market behavior and detect performance drift earlier across the trade lifecycle.