Key Takeaways

- Temporal hallucination occurs when AI gives an answer that may be factually correct but is wrong for the decision moment.

- In capital markets, stale or mistimed AI outputs can create mispriced risk, missed signals, regulatory exposure, and indefensible decisions.

- Standard RAG reduces some AI hallucinations, but it does not solve temporal validity because it ranks by semantic relevance rather than decision-time context.

- Temporal RAG combines time-series analytics with vector search so AI can understand not only what information is relevant, but when it was true.

- KX gives capital markets AI a trusted sense of time by unifying time-series and unstructured data in a temporal infrastructure designed for faster, explainable, and defensible decisions.

We’ve all experienced déjà vu: the unsettling sense that the present has somehow happened before. There’s also the lesser-known phenomenon of jamais vu, when a face, place, or even a word you know well can suddenly seem strange.

Both experiences show how dependent our sense of reality is on temporal order. We don’t simply recognize the world around us; we ground that recognition in time. When that sense of causality breaks down, our perception quickly becomes unreliable.

AI has its own version of this problem. I call it temporal hallucination — and it’s a dangerous failure mode no one is talking about or watching for in capital markets.

Temporal hallucination is when an AI model returns an answer that’s semantically correct but belongs to the wrong moment in time. A filing that was accurate last quarter. A risk signal from a different regime. A liquidity pattern that vanished an hour ago.

The answer looks plausible. Unlike the AI hallucinations everyone has learned to fear, it may even have been correct once. But in markets where decisions determine outcomes in milliseconds, a response that’s right in the abstract and wrong in the moment isn’t an answer; it’s a liability.

Temporal hallucination shows up as mispriced risk, missed signals, and decisions that can’t be defended after the fact. It’s an overlooked but critical AI failure mode that every capital markets firm needs to name, understand, and design infrastructure to prevent.

The world runs on decisions, not data

“The purpose of information…is being able to take the right action.” — Peter Drucker Austrian American management consultant and author

For years, the AI trust conversation has revolved around data. Do we have enough? Is it clean? Is it complete? Can we keep pace with the rising volume, velocity, and variety?

These are reasonable questions. Capital markets are absorbing a step change in message rates, sub-penny ticks, odd-lot integration, and near 24/7 trading, as well as an unprecedented expansion of alternative data.

But these questions also miss the point: the end goal isn’t better data — it’s better decisions.

Markets don’t reward firms for storing more, validating better, or querying faster, unless those gains translate into better action. Data becomes a competitive moat only when it is structured, sequenced, and temporally faithful enough to support the right decision at the right moment: when to trade, when to adjust exposure, when to escalate risk, and when to do nothing at all.

This is what I mean when I say ‘data is the algorithm’: the model is no longer the differentiator. The temporal structure of the data the model is trained on, grounded in, and evaluated against is what separates a firm that acts in time from a firm that arrives too late. And, in capital markets, late is expensive.

Truth has a shorter half-life than ever. Commoditized models and generic AI capabilities mean the decision window to go from signal to action is narrowing by the hour, not the quarter. It’s survival of the fastest.

The stakes climb again as AI moves beyond advisory tools into agentic workflows, from retrieval and analysis into autonomous decision-making. An LLM giving a stale answer creates confusion. An agent acting on stale context creates financial, regulatory, and reputational damage.

Every agentic AI deployment in capital markets is, whether a firm realizes it or not, a bet that temporal hallucination has been engineered out of the stack.

Engineering temporal integrity

“Being right too early is indistinguishable from being wrong…” — Christopher Ailman, Former CalSTRS CIO

Most temporal hallucinations aren’t model failures; they’re infrastructure failures.

In general-purpose databases, time is often treated as an attribute, a timestamp added to a row. In temporal AI infrastructure, time is the organizing principle. It determines what happened, in what order, what was known at each moment, and whether a fact still applies.

A price movement means little without the sequence of orders that caused it. A credit rating means little without knowing when it was issued, when it was recorded, and whether it has been superseded. A client preference means little without knowing whether it preceded or followed the last trade, the latest call, or the most recent market shock.

This is the essence of bi-temporal integrity: tracking both valid time, when a fact was true in the world, and transaction time, when the system recorded it. Without both, AI cannot reliably know what was true, when it was true, and what changed next. That makes temporal hallucination not just a risk, but a property of the system.

A firm with bi-temporal integrity can answer questions a competitor cannot even ask. Did the model see the news before it acted? Was the position taken when the signal was still fresh? Can we reconstruct, on demand, what was knowable at 09:31:04 on a given morning?

These are the questions regulators, auditors, and risk committees are starting to ask. They are also the questions every capital markets firm will eventually need to answer in production, at speed.

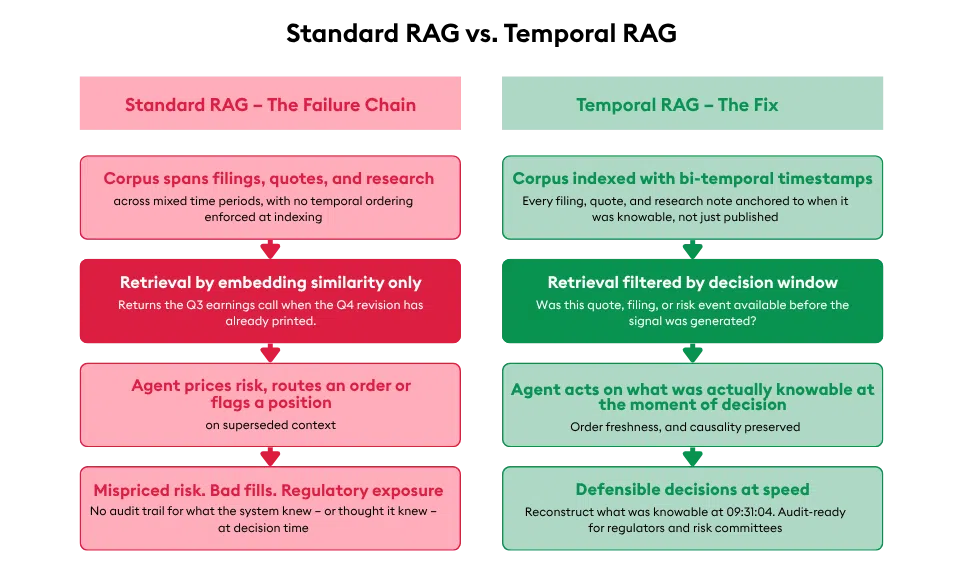

Standard RAG can’t fix the problem

“What was most important…was knowing how to react appropriately to the information available at each point in time.” — Ray Dalio, American investor

Retrieval-augmented generation has become the default answer to AI hallucination, grounding model outputs in documents, records, and data sources.

But standard RAG operates by semantic relevance, not temporal validity, and it wasn’t designed for markets where context decays by the second. In fact, it can deepen temporal hallucination — surfacing the right-looking document while missing whether the world has moved on.

The fix is temporal RAG, which doesn’t just ask whether a document is relevant but whether it belongs to the right decision window. Was this information available when the decision was made? Did it arrive before or after the signal? Was it superseded by a newer filing, quote, chat, or risk event?

By combining vector search with time-series analytics, temporal RAG lets AI reason across structured market events and unstructured language while preserving order, freshness, and causality. It’s the difference between an AI that knows the answer and an AI that knows when the answer was true.

Look-ahead bias is the silent driver of temporal hallucination

Every quant knows look-ahead bias. It is the cardinal sin of strategy development: using information in your model that would not have been available at the moment of decision. A price that had not yet printed. A filing that landed tomorrow. A correction issued next week.

Look-ahead bias has been a discipline problem in quantitative finance for decades. AI has turned it into an infrastructure problem.

The reason is simple: AI doesn’t just consume historical data. It trains on it, retrieves from it, reasons over it, and increasingly acts on it. Every one of those stages is a potential point of leakage.

A model trained on a corpus that mixes timelines learns the future. A RAG pipeline that pulls the current version of a filing instead of the version that existed at decision time gives the agent hindsight it should not have. An agent that retrieves the latest data rather than what was knowable at a point in time is, by construction, hallucinating temporally.

Regardless of where the leakage happens, the result is the same failure mode. An AI system that appears to outperform in development, fails to generalize in production, and produces decisions no one can defend after the fact. In a backtest, look-ahead bias inflates returns. In an AI agent, it inflates confidence in answers that were never really earned.

Eliminating this requires more than careful coding. It requires infrastructure that knows when every fact became true, when the system recorded it, and what version was available to whom at any point in the past.

Without that substrate, every AI workflow in capital markets is structurally one query away from look-ahead bias.

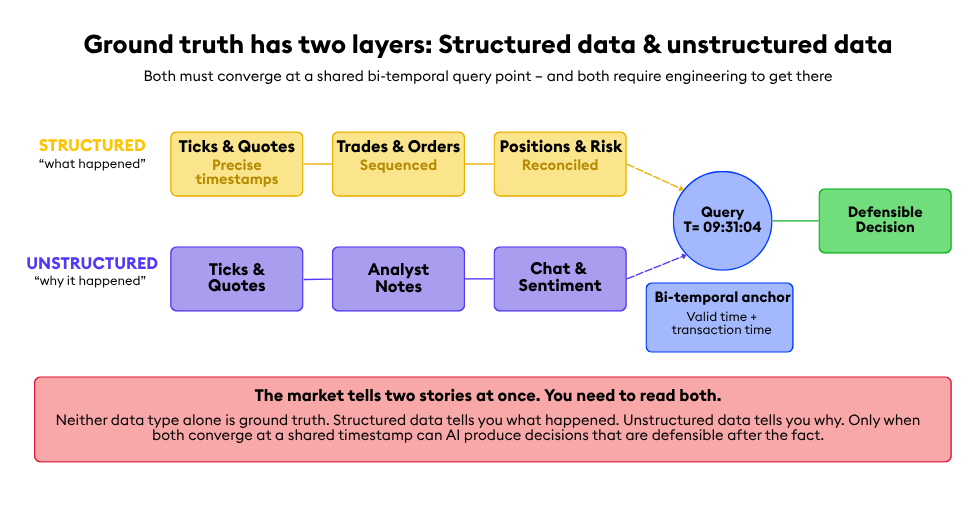

Ground truth has two layers

“We are in fact creating a whole new industry to support AI factories, AI agents, and robotics, with one architecture” — Jensen Huang, NVIDIA CEO

Markets have never been describable in a single data type.

Structured market data tells you what actually happened: every tick, trade, quote, order, position, and execution — timestamped, sequenced, and reconciled across venues, symbology, and corporate actions. This is the record of the world as it was.

Unstructured data tells you why it happened, what people thought was happening, and what they expected next: news, research, filings, analyst commentary, earnings transcripts, client emails, chat, and sentiment. This is the record of what was knowable, by whom, and when.

Neither alone is ground truth.

A model that sees only structured data sees the market move without the cause. A model that sees only unstructured data sees the narrative without the price. AI that reasons across both, anchored to time, sees what humans see when they make good decisions: the event, the context around it, and the sequence that connected them.

This is the harder engineering problem in temporal AI, and it is where most stacks break. Structured time-series and unstructured semantic data have historically lived in different systems, with different query models, different latencies, and different notions of time. Joining them at query time, at production speed, with bi-temporal fidelity is what separates a temporal AI platform from a database with a timestamp column.

The question Wall Street needs to answer now

Every major bank, asset manager, and hedge fund is facing a similar challenge. Structured and unstructured data sit in separate silos. Teams spend hours rebuilding context that the system should have served in seconds. The AI strategy is written, but the foundation underneath it is missing.

KX is the temporal AI infrastructure that closes this gap. For 30 years, we’ve been Wall Street’s secret weapon, powering the world’s most demanding trading systems.

KDB-X gives AI a sense of time, unifying structured time-series and vectorized unstructured data in one engine, with the bi-temporal discipline that makes look-ahead bias an engineering property of the system rather than an analyst’s problem. OneTick Market Data strengthens that foundation, turning fragmented exchange and vendor feeds into a governed, query-ready substrate for research, analytics, and AI workflows.

Together, they give capital markets firms a single temporal foundation from which to build, decide, and defend.

The urgent question for capital markets is no longer whether AI can tell the truth — it’s whether AI can also tell the time. Until firms can answer that, every AI decision they deploy is one timestamp away from a temporal hallucination they won’t see coming.

Don’t be blindsided by AI déjà vu. See why the world’s leading firms with more than $50 trillion in assets under management rely on KX’s temporal AI infrastructure to turn raw data into trusted decisions at the speed capital markets demand.